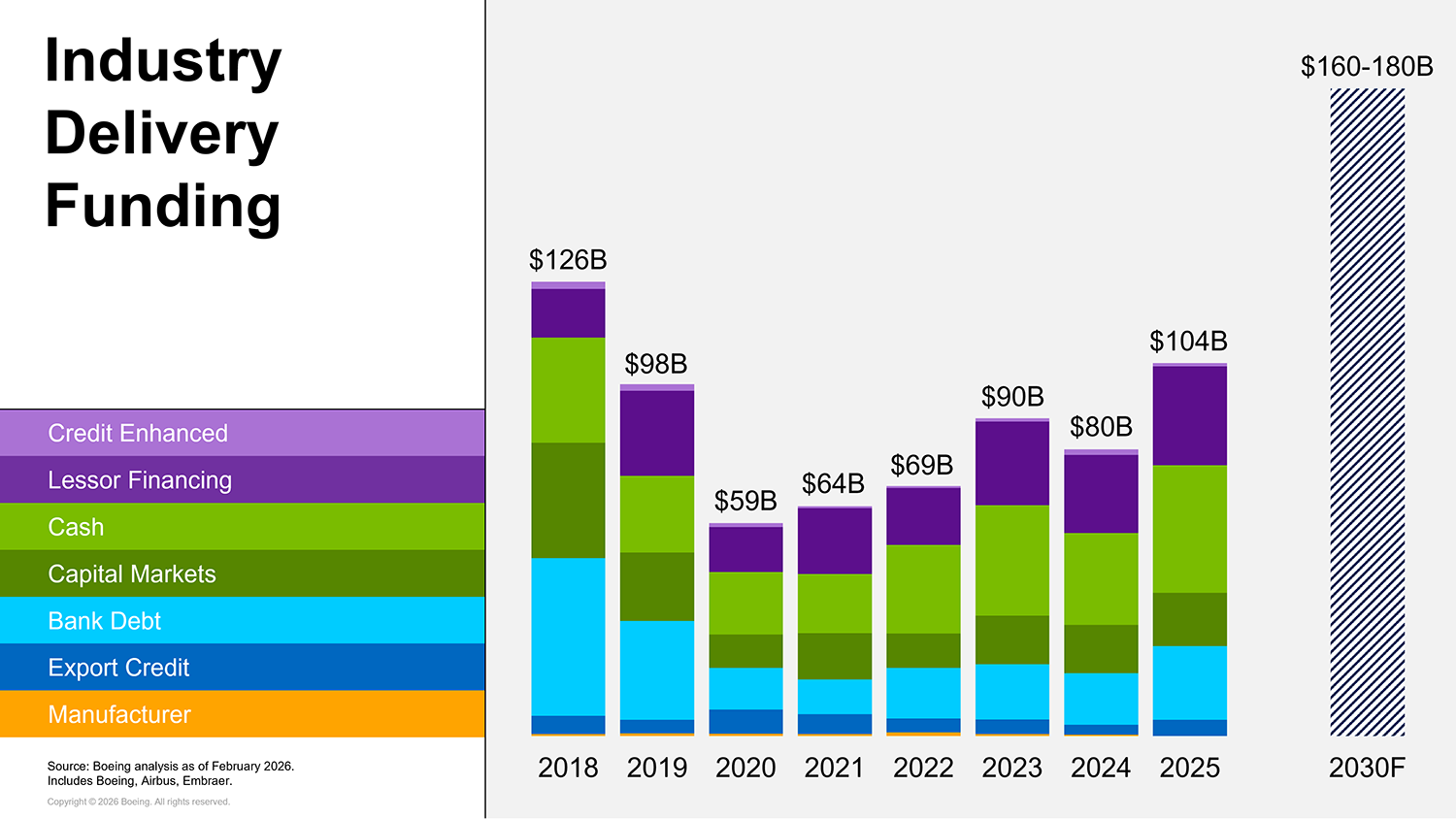

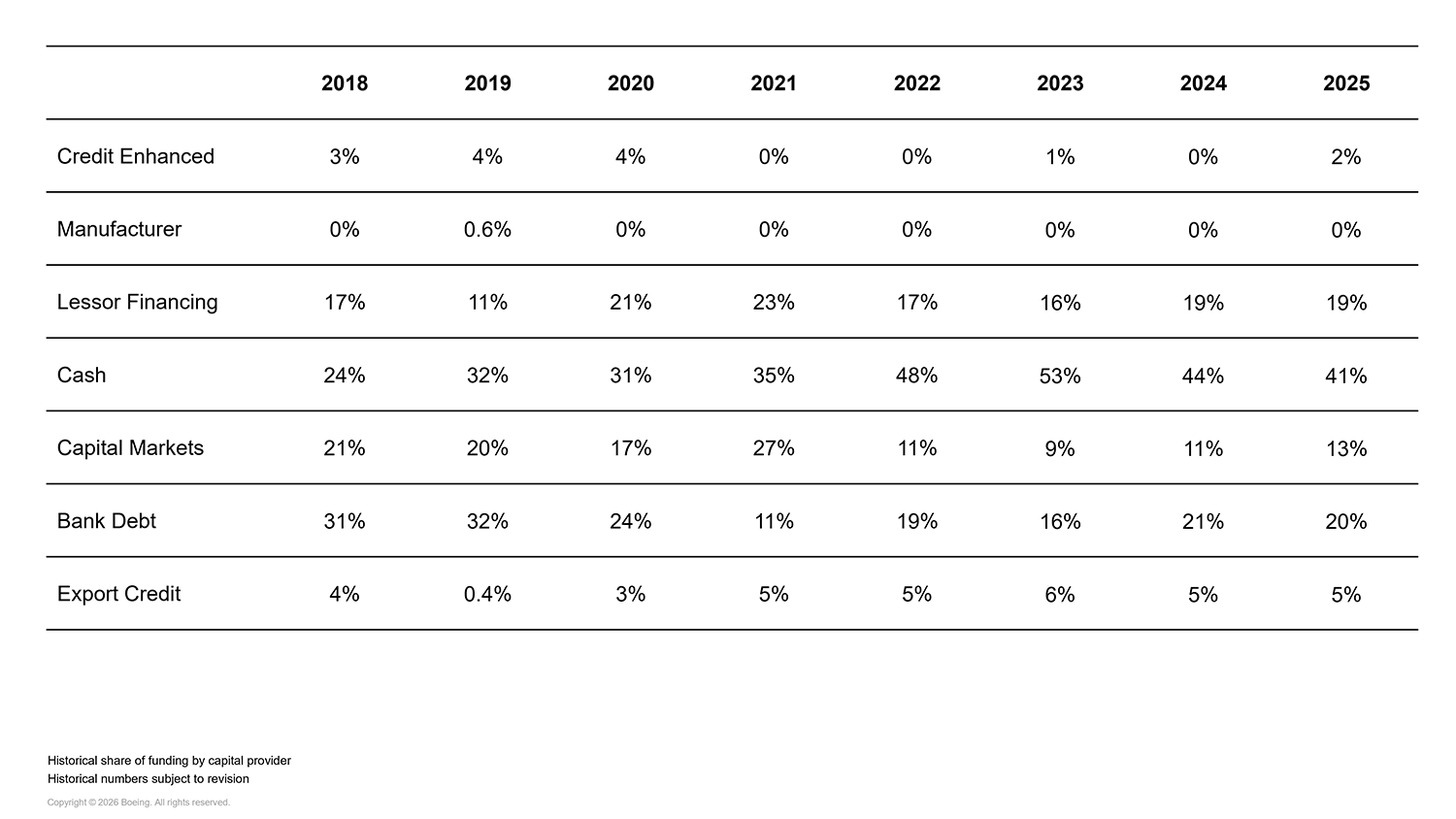

A more robust OEM aircraft delivery stream year over-year brought a healthier pool of financing opportunities to the markets, but yields for many transactions remained stubbornly low through the course of 2025. That tight pricing has continued into 2026.

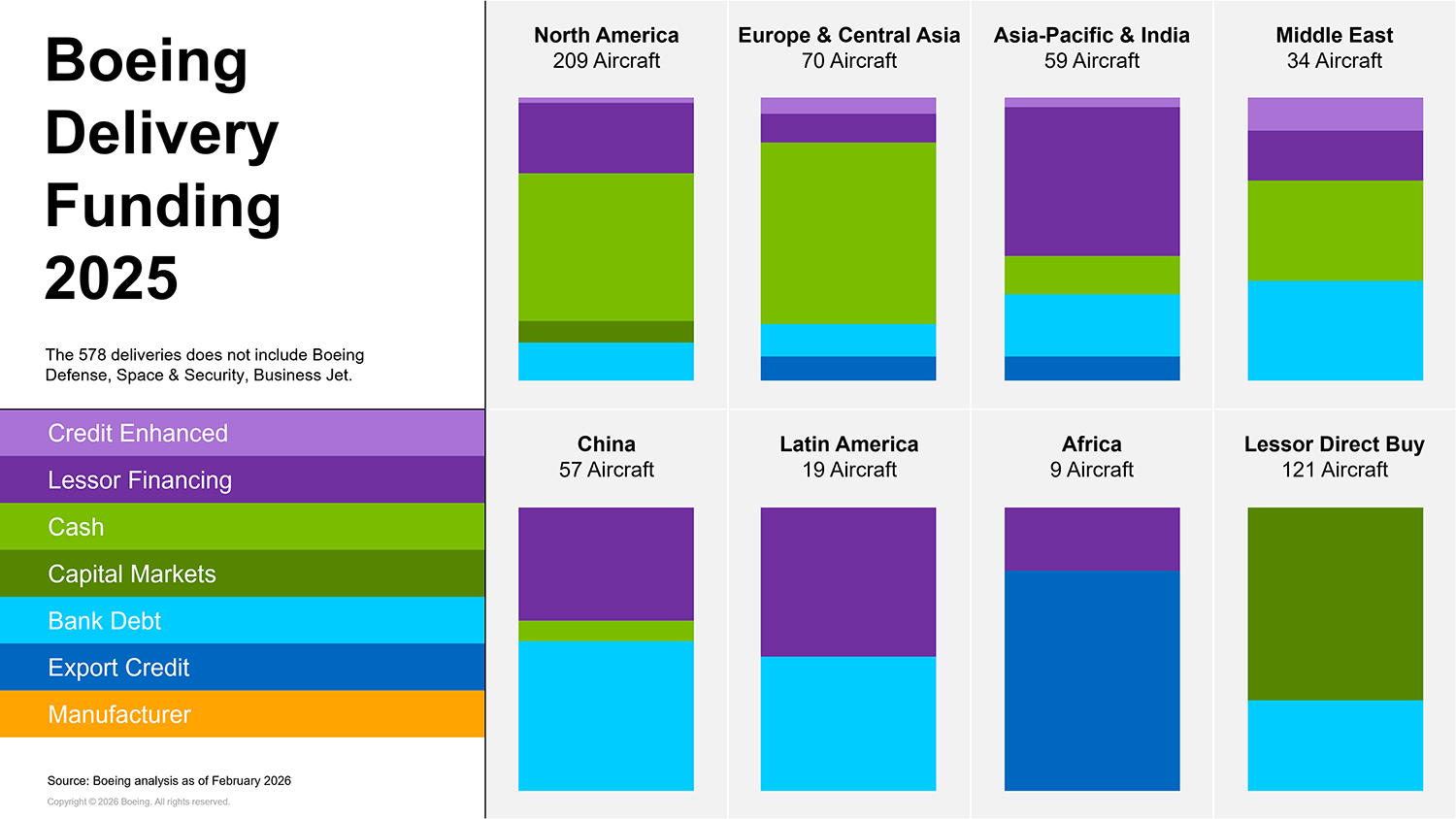

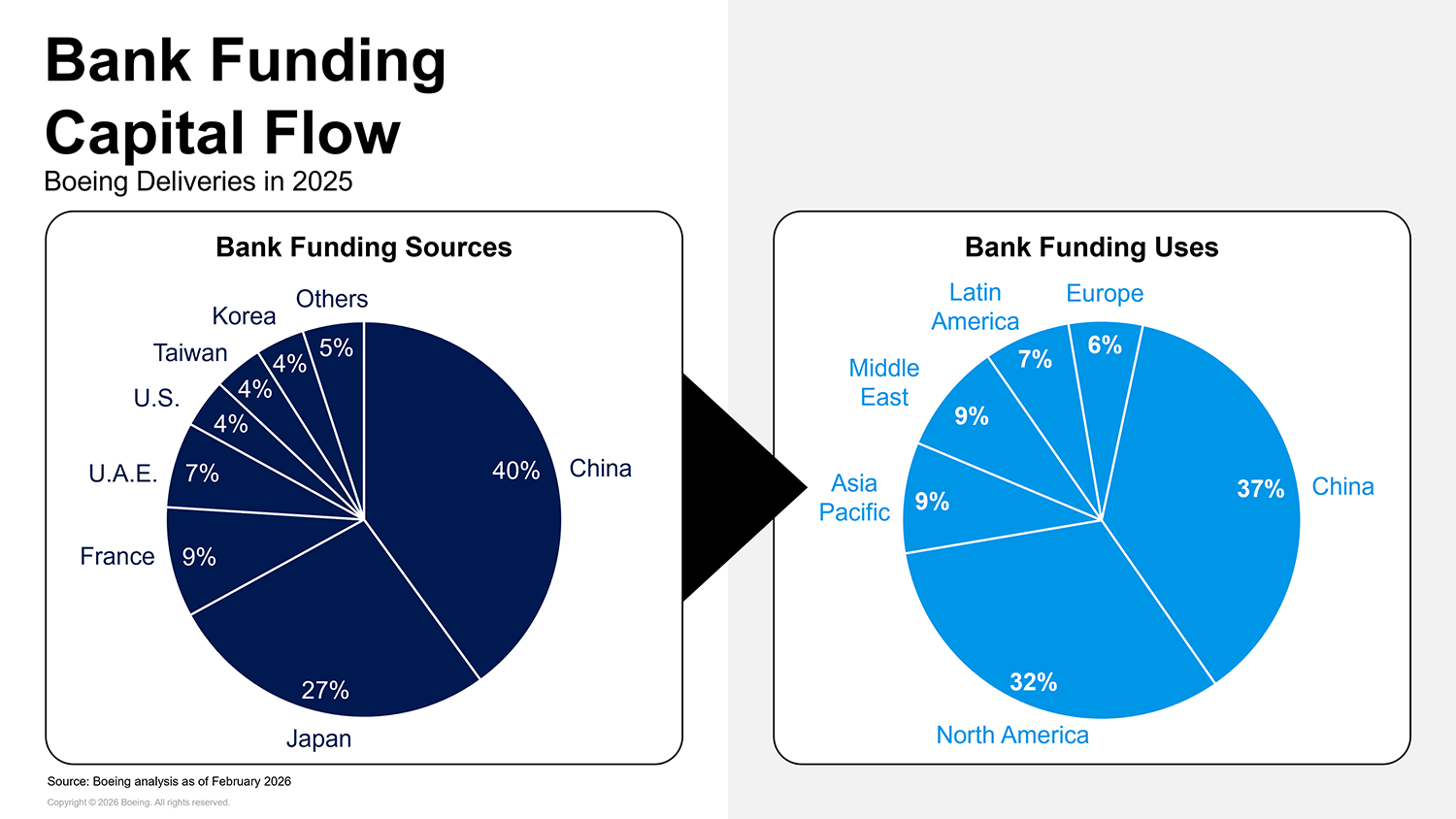

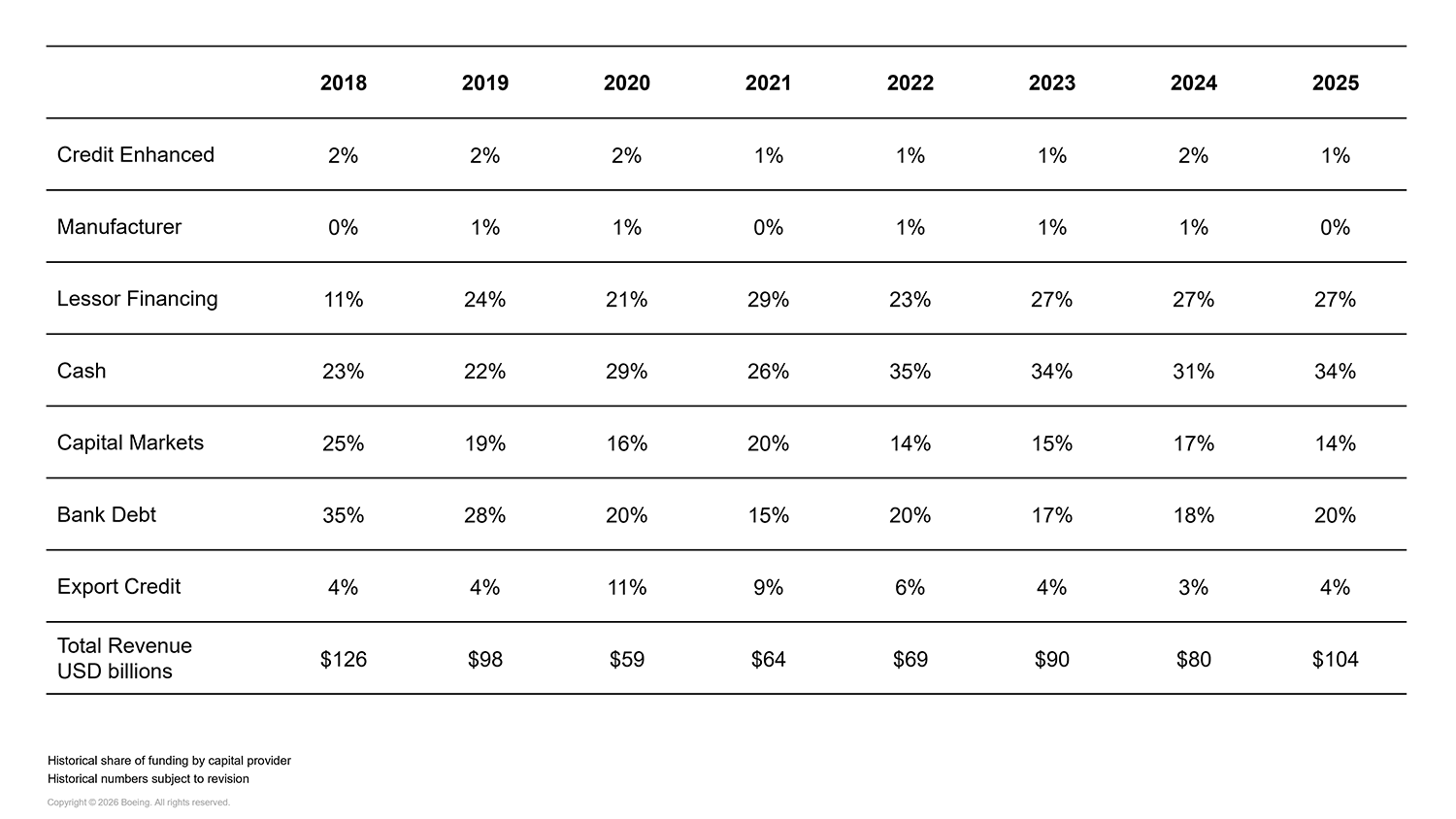

Diversity of funding sources was a hallmark of 2025, and this product optionality prevented any single capital source from unduly dominating the financing marketplace. Very strong offerings from the private sector in the North American markets, for example, continued to temper public asset‑backed issuances by U.S. airlines. We have also observed a number of private financing platforms continue to develop their product offerings, often blurring the lines between credit and asset financiers. This financing kaleidoscope was further reinforced by alternative lenders deploying different pockets of capital through their associated vehicles, enabling airlines to create bespoke solutions for their delivery financing requirements. Regional capital, notably from the Middle East, is engaging both within its corridors and on the international stage. It appears that new financings will be eagerly competed for through 2026.

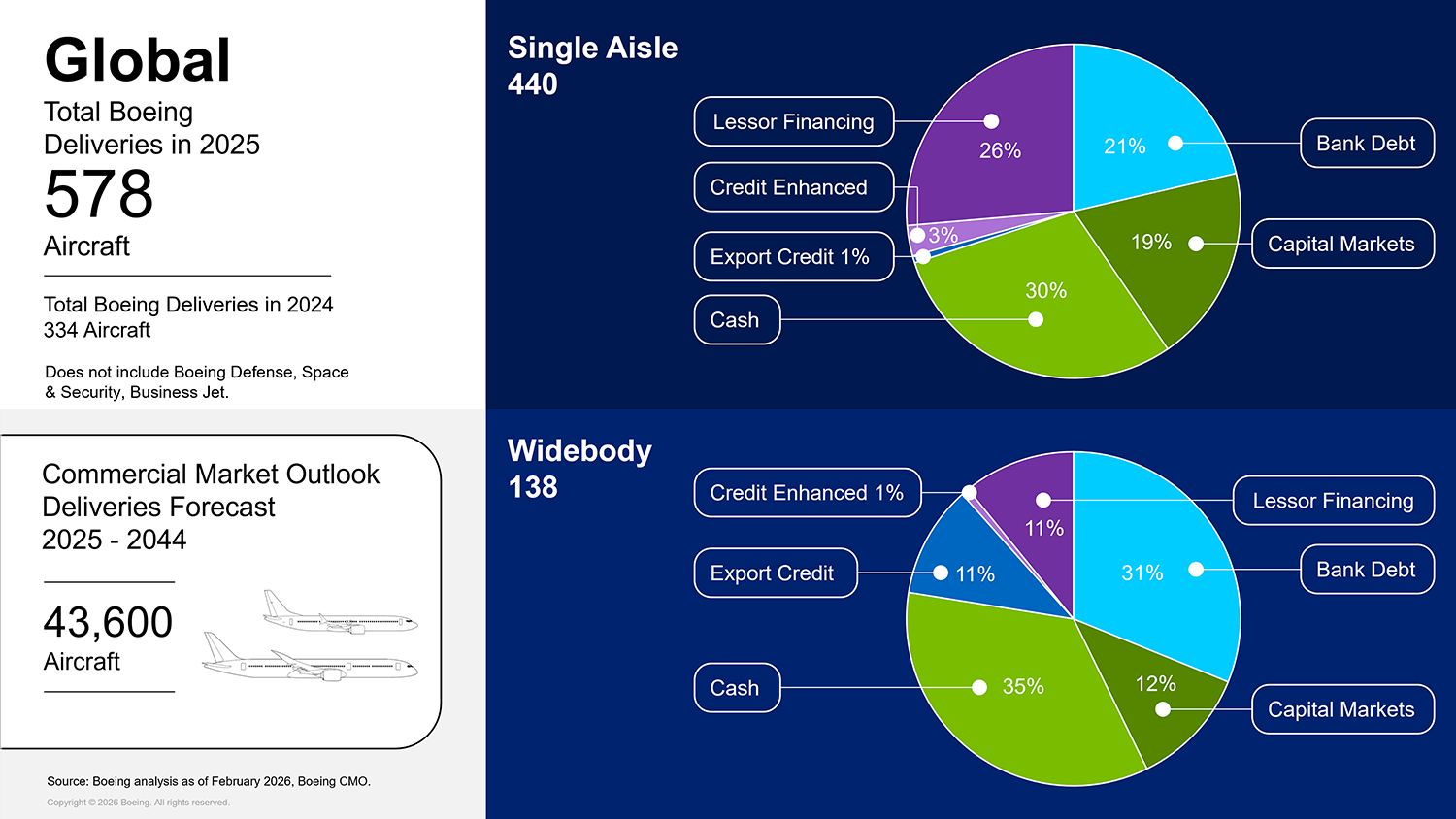

As with all big-ticket financings there will be natural exposure limits reached per institution and consequently a need to actively manage portfolios. Distribution and syndication activity continues to increase as new aircraft deliveries (notably widebodies) pick up year over year and thoughtful horizon planning around financial product selection will be instrumental in securing ongoing capital availability for airlines.

We expect funding requirements continuing to grow through the decade (and beyond), which reflects the strong OEM order books and expectations of increased production levels. The outlook for new financing volumes in this period (2026–2030) is forecast to be materially higher than previously seen and will require all primary financial products to be operating satisfactorily to meet new delivery volumes.